Important Highlights:

Tampa Bay:

- Within the last 5 quarters, office space leasing has been increasing rapidly.

- Tampa Bay Wave ranked #1 in Florida for the organization with the greatest number of startups receiving investments!

- The unemployment rate in Tampa Bay increased to 5.0% in October 2021, compared to the end of 2nd Quarter 2021, which was approx. 4.6%.

- Average direct asking rentals are down 2.5 percent year over year, owing mostly to re-pricing in certain availabilities that have been on the market for more than a year. In contrast, several Class A buildings in Westshore raised their asking prices to $42.00 per square foot, bringing them closer to pre-pandemic values.

- For the sixth year in a row, Florida has been rated first in net migration. According to the United States Census Bureau, Florida gained the most inhabitants between July 2019 and July 2020, with 252,717 additional residents.

Office Market:

- Office vacancy rates increased in Hillsborough County and Pinellas County to around 12% but have remained fairly constant.

- Both Class A and Class B building’s rents grew more than 2%, placing Tampa in the top 15 markets in the US with average office rentals of more than $25 per square foot.

- Absorption trended negative for the quarter and remains negative year-to-date, but several submarkets recorded positive quarterly absorption.

- Westshore submarket which leads in year-to-date absorption with over 140,000 s.f. Nearly all the quarter’s negative absorption took place in the Northwest Tampa submarket.

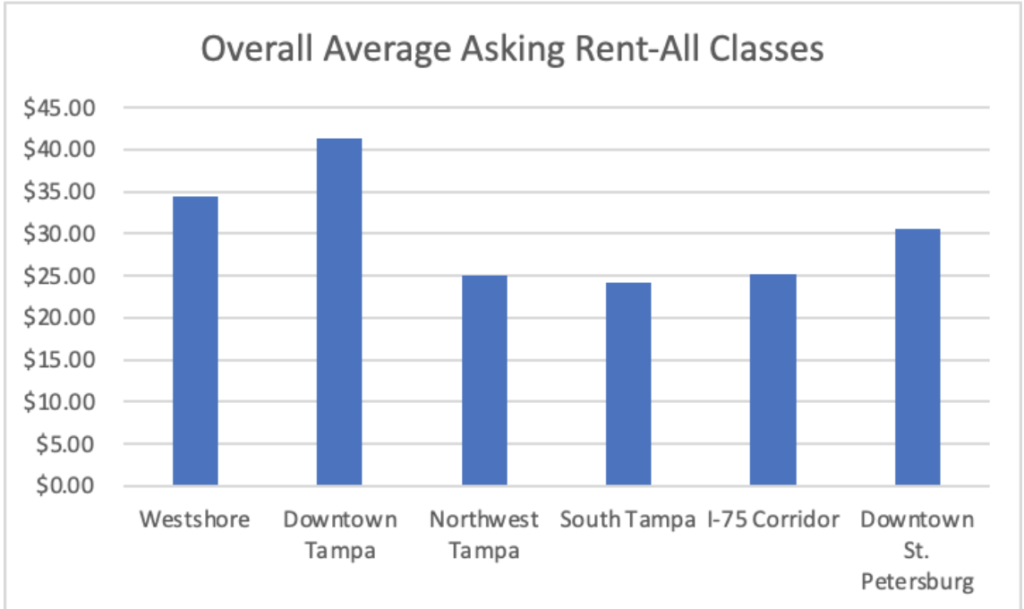

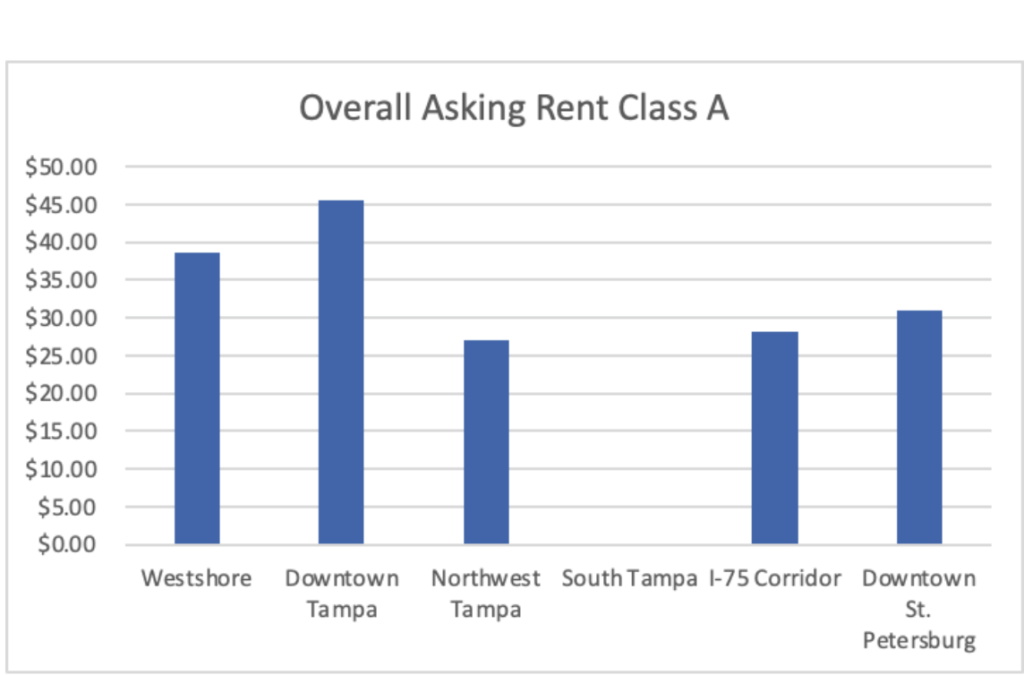

Let’s Talk Rent Numbers:

| Submarket | Overall Average Asking Rent-All Classes | Overall Asking Rent Class A |

| Westshore | $34.42 Sq. Ft. | $38.57 Sq. Ft. |

| Downtown Tampa | $41.26 Sq. Ft. | $45.48 Sq. Ft. |

| Northwest Tampa | $24.96 Sq. Ft. | $27.11 Sq. Ft. |

| South Tampa | $24.16 Sq. Ft. | N/A |

| I-75 Corridor | $ 25.19 Sq. Ft. | $28.23nSq. Ft. |

| Downtown St. Petersburg | $30.55 Sq. Ft. | $30.88 Sq. Ft. |

Construction Highlights:

- The 380,000 s.f. was completed this quarter at 1001 Water Street in Tampa. Additionally, 500,000 s.f. was delivered earlier this year at SkyCenter One, Midtown West, and The Lofts at Midtown, all in the Westshore submarket.

2021 4th Quarter Forecast:

- Confidence in the Tampa Bay market is high, going into the last quarter of 2021 and into 2022 amid sustained new-to-market tenancy.

- Total vacancy is expected to remain the same through the rest of 2021

- Tenants will slowly proceed to bring their teams back to the office

- By mid-2022 remaining new construction space with many buildings is expected to be over 50% leased.

What does this mean for Tenants?

- Managing market expectations of primary markets that are experiencing higher office vacancies than Tampa Bay. Landlords in Tampa Bay are not motivated in the same way that they are in other parts of the country to replace vacancies due to the lower vacancy rates than primary markets such as New York and Los Angeles.

- Take advantage of market circumstances we do have by making use of available sublease space, which can offer more reasonable rates, shorter terms, and any available furniture.

What does this mean for Landlords?

- Evaluate concessions for Tenants by adjusting asking rents, higher Tenant Improvement allowances to gain a competitive edge over Landlords who maintain their face prices

- Provide more flexible lease terms

- Expect an increase of new to market Tenants are expanding or relocating to Tampa from other states

- Start marketing available space 6 with a longer advanced lead time for office space that is coming available